Description

Business Overview:

- Medpace is a contract research organization (CRO) for clinical trials that differs from larger publicly traded CROs in its narrow focus on (a) small and mid-cap biotech sponsors, and (b) exclusively offering the full-service outsourcing (FSO) model to customers.

- In 2025, 95% of Medpace revenue came from small and mid-sized biopharma (82% and 13% respectively).

- There are two business models in the CRO space – FSO and FSP (Functional Service Provider). Large public CROs like IQVIA and ICON do both, but their work for large pharma clients is often FSP, where they function as outsourced labor handling certain administrative/labor-intensive parts of the trial process. Medpace exclusively does full service outsourcing and handles all aspects of the clinical trial for the sponsor, including strategic areas requiring specific expertise like planning the design of the trials and regulatory strategy for the IND (Investigational New Drug).

- We’ll discuss AI more later, but our view is that the FSO model + working with smaller biotechs insulates Medpace from AI risk relative to the other publicly traded, larger CROs.

- Medpace was founded in 1992 by August Troendle, who remains CEO and deeply involved in the day-to-day operations of the business. He owns ~20% of shares outstanding. August is 69, but there are no signs of him stepping back in the near to medium term.

- Medpace has a “top-down” culture – this is August’s business. While you will read a lot of poor reviews on sites like Glassdoor about August and Medpace’s culture, our discussions with higher-level formers have been more balanced, and August’s track record at growing the business efficiently + capital allocation has been extraordinary. Medpace is an intense place to work, with revenue per employee significantly higher than other public CROs (partly because of the business model – Medpace employs many MDs/PhDs who are true experts in their field, whereas large CROs have a higher proportion of lower-level staff, but also partly because of the culture / intensity of the organization).

- Medpace revenue per employee is substantially higher than the large public CROs, and the gap is growing wider over time. As of 2025, Medpace revenue was $408K/employee vs. IQVIA at $175K and Fortrea at $190K, so Medpace was over 2x higher than the large CROs. In 2021, Medpace was at ~$254K vs IQVIA at $176K, so Medpace has managed to grow rev/employee ~60% in four years while IQVIA has not grown at all.

- The drug development process is long and expensive, and the trial process is make or break for Medpace’s core customer, who might be a company with a single drug candidate. This underscores the importance, especially for this customer type, of picking the “right” CRO who can get the job done properly.

- After a biotech discovers what they think is a compelling molecule, preclinical work occurs to evaluate safety and efficacy. For example, this could include animal testing, although animal testing is declining in popularity. Medpace is not involved in preclinical work. CRL (Charles River Laboratories) is a publicly traded preclinical CRO. While not a focus of our research, our work suggests preclinical work could be more susceptible to AI disruption/optimization, which could be good for Medpace (as it should speed up the process of getting drugs to the clinical stage, where Medpace is involved).

- Medpace gets involved at the Clinical stage - testing in humans. The first step in this process is designing the clinical development program / plan for the clinical trials.

- Phase I of clinical trials involves testing, often in healthy volunteers, for dosage, safety, interactions, etc. Phase I is by far the smallest part of the trial process in terms of scope / revenue for Medpace, but ideally, Medpace wins a customer for the entirety of their clinical trial process.

- Apple DCF

- Netflix DCF

- Microsoft DCF

- Facebook DCF

- Tesla DCF

- Amazon DCF

- Apple WACC

- Netflix WACC

- Microsoft WACC

- Facebook WACC

- Tesla WACC

- Amazon WACC

- Apple Intrinsic Value

- Netflix Intrinsic Value

- Microsoft Intrinsic Value

- Facebook Intrinsic Value

- Tesla Intrinsic Value

- Amazon Intrinsic Value

- Phase II is where the trial gets more complex, involving dozens or hundreds of clinical sites globally where the drug is tested in patients. At this stage, you are trying to figure out if the drug works and at what dose. Medpace has relationships with sites around the globe and depending on the drug candidate (i.e., how niche it is), Medpace may need to get creative in finding the right sites / test patients for the study.

- Phase III is a further step up in complexity / revenue for Medpace, involving hundreds of sites and typically randomized, double blind studies. The bulk of trial revenue for Medpace is in Phase III. The goal is to prove the drug works at scale with the statistical rigor required for regulatory approval.

- After a successful Phase III, Medpace will assemble the full data package from the trial process into the format required by the FDA or other authorities. An FDA review will then occur, and Medpace will handle responding to FDA queries.

- After a drug is approved and enters the market, the engagement may continue. Post-marketing safety studies, testing the same drug for new indications, etc. are some of the activities Medpace may help with after a drug is in the market.

- Medpace has expertise in many clinical areas, but is particularly strong in oncology and metabolic trials. Metabolic has been a fast-growing segment of the market. In 2025, metabolic trials were 29% of revenue for Medpace, the second largest therapeutic area behind oncology at 30%.

Thesis Summary:

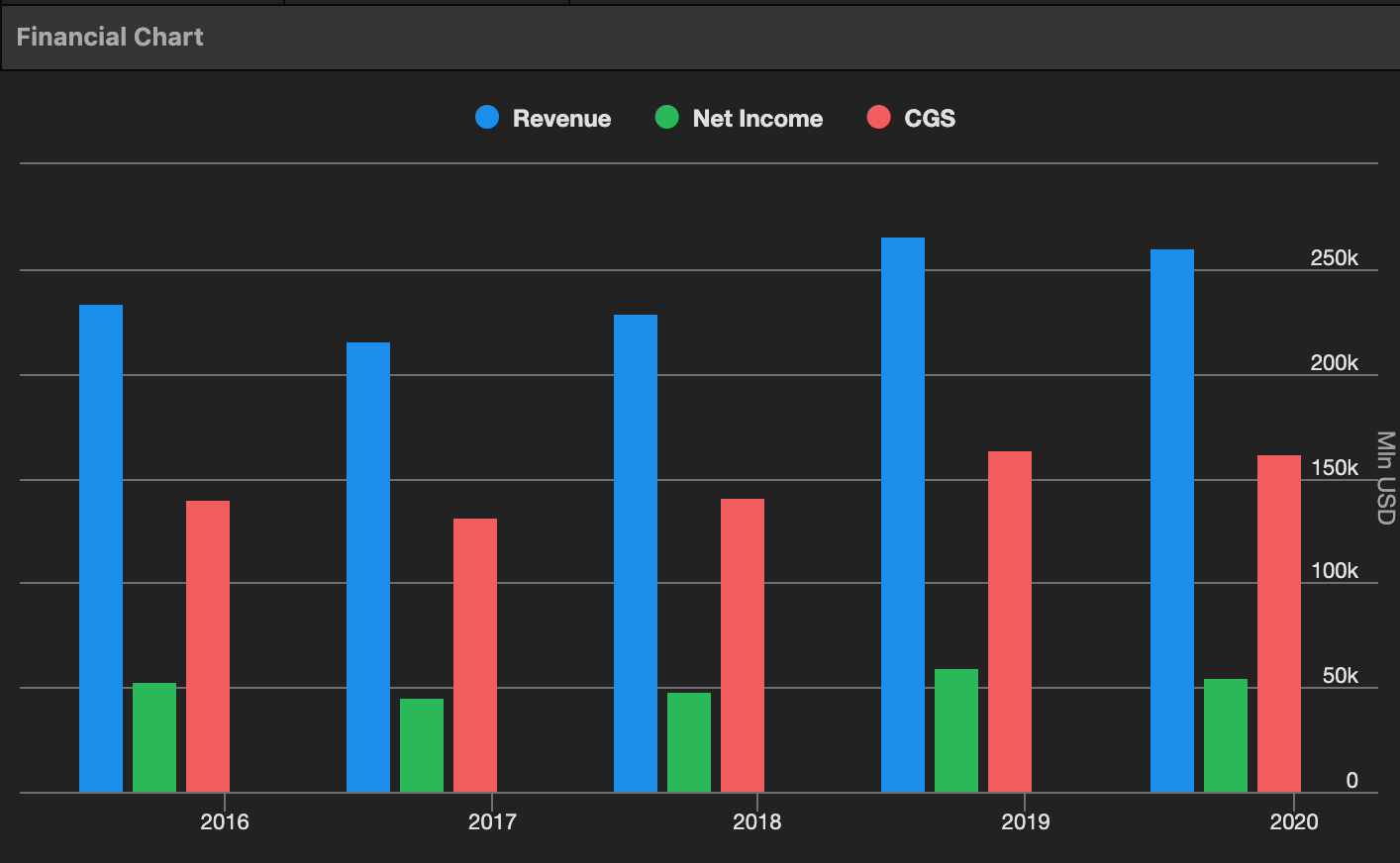

- Medpace is a structural share-gainer / winner in the fastest (over the long-term) growing segment for clinical trial demand, small-to-mid-sized biopharma. As of 2024, Medpace had an estimated market share of ~7% for small and mid-sized biopharma clinical trials. The small to mid sized biopharma CRO market (clinical trial spend * outsourced percentage) is estimated to be ~$29 billion as of 2024 vs. Medpace revenue of $2.1 billion. In 2025, Medpace’s revenue was $2.5bn, up 20% YoY, so it’s likely Medpace’s share is now ~8%. We think there is a long runway for both the industry to grow HSD%+ and Medpace to continue to gain share, driving mid-teens or higher revenue growth over an extended period of time.

- From 2019-2025, Medpace has grown revenue at a ~20% CAGR from both TAM expansion and market share gains. In 2019, Medpace’s share of the market was ~5%. Roughly, we estimate the small to mid sized biopharma CRO market has grown ~10%/yr from 2019-2025, so market growth and market share growth have been roughly equal contributor’s to Medpace’s 20% revenue CAGR.

- Our work suggests it’s likely the small to mid sized biopharma market will continue to grow at a high rate, similar to or potentially above historical levels. In addition to the funding environment improving over the past year and positive demand signs in government clinical trial data to start off 2026 (see point #4 below), there is a reasonable argument that AI advancements will accelerate the drug development process and likely also the preclinical timeline. This seems like a near-certainty over time, but whether it’s relevant for our investment time horizon in Medpace (which we underwrite to a ~5 year hold) is less obvious. But it is plausible that by the end of this decade, we start to see signs of an acceleration in the top of the funnel for Medpace.

- We expect Medpace’s market share to continue to grind higher. At a high level, our work suggests that Medpace’s focus on being the best possible partner to one slice of the market (small to mid-sized biopharma, FSO model), as well as its owner-operator culture, allows Medpace to out-execute peers even though Medpace lacks the hard, tangible competitive moat that we look for in most investments.

- An example we’ve heard of the difference in culture at Medpace vs large CROs is the way they handle pitching to potential clients. When Medpace is meeting with a prospect, they will bring the actual team who will work on the client if they select Medpace, including experts in the therapeutic area, to the meeting – whereas a big CRO will probably be sending a sales executive / team. For a biotech company with a few employees, who are themselves largely technical experts, meeting with the actual team they’d be partnering with (the FSO model is effectively a partnership) who can speak their language is compelling.

- Large CROs have an incentive to put their “A” team on big, large pharma clients. A small biopharma company is more likely to be confident that Medpace will dedicate the necessary resources to their trial than with a large CRO.

- Another example of Medpace’s culture is that they don’t choose to bid on all projects. Biz dev employees at Medpace have to pitch the opportunities they’ve found at a daily 10 AM meeting that includes August Troendle (CEO) and Medpace’s medical directors and heads of each therapeutic area. If Medpace isn’t confident in the funding that the potential client has, if it’s an early stage trial and Medpace doesn’t believe the IND will be successful, (a Phase I trial is low revenue, so taking on a Phase I client is a bet that they’ll make it to Phase II/III), or if Medpace believes the potential client has unrealistic expectations about the trial scope/timing/cost, they will decline to bid. In an industry where the failure rate of biopharma companies/trials is very high, having the discipline to turn down business is a real advantage to maximizing productivity.

- There is a flywheel effect in the CRO industry. Medpace is now known in the industry as a leader in metabolic, oncology, and complex / difficult trials in general (i.e., ones where it is difficult to find a patient population large enough – i.e. rare diseases). They have a ton of case studies of successful trials in these areas, they have leading experts on staff, and as a result, a biopharma team with an IND in those sectors, betting their company on the outcome of the trial, is more likely to pick Medpace than a CRO with less experience.

- Medpace offers customers a fixed price for the trial – Medpace takes the risk of the trial ending up being more expensive than originally anticipated. This isn’t completely unique in the industry, but large CROs are generally not guaranteeing a fixed price, and we’ve heard other CROs are known for more frequent change orders. For a biopharma company with limited, and likely fixed, funding, being quoted a fixed price upfront is valuable.

- We have strong alignment with August Troendle given his ~20% ownership stake, and Medpace is run with expense and capital allocation discipline.

- Medpace’s incremental margins have been very impressive. The margin expansion in the business is somewhat obfuscated by trends in pass-through expenses, which are high in certain types of trials (e.g., metabolic). While Medpace’s reported EBITDA margin is up from ~17% in 2019 to ~22% in 2025, when you strip pass-through expenses out of revenue and costs, the EBITDA margin on net revenue has gone from mid-20s % in 2019 to high-30s % today. Net revenue growth has been ~3 points slower than gross (reported) revenue.

- Medpace has cost advantages vs. a typical CRO due to its location in Cincinnati, a relatively low-cost area, and its practice of largely hiring and training fresh graduates.

- Medpace returns cash to shareholders via buybacks and has a track record of being aggressive with buybacks when the stock is cheap. In 2025, Medpace repurchased ~3mm shares (~10% of shares outstanding) and nearly all of these repurchases came in Q1 and Q2, when the stock price was low (~$300).

- Medpace has a net-cash balance sheet with ~$497mm of cash and no debt as of YE ’25, for net cash per share of ~$17.

- While it’s difficult to be certain, our guess is that AI is more of a tailwind than a headwind for Medpace, at least with a 5 year horizon.

- It seems likely AI will accelerate the top of the funnel, as discussed above – the number of new molecules entering the pipeline will likely grow, the preclinical timeline will likely be somewhat compressed, and the success rate of new molecules will likely be higher. The timeline for all of this to play out is unclear, but there are some very early signs of AI-aided drug discoveries entering the pipeline.

- It seems much less likely that AI, for the foreseeable future, will meaningfully change the structure of the clinical trial process. The process of testing drugs over multiple phases in human subjects, including blind trials, is likely to remain the default process for a long time.

- We expect AI to reduce the administrative burden of running a clinical trial. For example, the work assembling reports and performing statistical analysis will likely be accelerated by AI with human review. That said, we’ve heard that there is very minimal AI use in the CRO process today, even in areas where the AI models may be capable – we’ve heard sponsors are reluctant to allow AI usage out of fear that it may draw more scrutiny in the regulatory review process at the end of the trial. It simply isn’t worth it to be among the first INDs that leveraged AI in preparing materials for FDA review. But we expect this concern to fade as AI models continue to improve & as time passes and AI use becomes more accepted.

- Our best guess at the future of the CRO industry is that revenue will decline, but costs will also decline. The areas where AI saves money will be the lower value, less complex areas of the trial. The areas of the work where Medpace provides the most value (therapeutic expertise, designing / planning a trial to ensure the right patient populations/sites and that it’ll be rigorous enough to pass FDA scrutiny, etc) seem unlikely to be impacted by AI in the foreseeable future.

- It seems highly unlikely that biopharma clients will in-source the process of running a clinical trial. Biotechs are lean teams that lack the relationships with sites, relationships with regulators, and regulatory / trial design expertise. Trying to save money by avoiding a CRO is likely a poor bet for a biopharma sponsor betting their company on the outcome of the trial.

- Medpace has sold off in the first two months of 2026 due to a combination of tepid book:bill (1.04x) in Q4 ’25 and AI fears, despite healthy 2026 guidance (adjusted for historical conservatism). Early signs from government clinical trial data (imperfect, and to be taken with a grain of salt) seem to be lining up with management’s guide, suggesting a strong 2026 and lower industry cancellation rates than we saw in Q1 and Q4 ’25. At $440, the stock trades at ~21x ex-cash our 2026 EPS estimate for a business that we expect has a runway to grow EPS >20%.

- 2024 – early 2025 was a difficult period for biopharma, but we began to see signs of a recovery in the funding environment in 2025.

- In 2025, Medpace noted a high rate of cancellations in Q1, but then saw much healthier book:bill in Q2 and Q3. On the Q4 call, a return to higher than expected cancellation rates was blamed for the tepid book:bill of 1.04x, with management noting healthy gross bookings offset by cancellations. Note that cancellation trends seem to be largely or entirely industry driven – in general, these are not clients leaving Medpace for a different CRO (switching costs are high), but rather companies that ran out of funding or where continuing the trial no longer makes sense. In cases when funding is threatened and a sponsor is at risk of not paying, Medpace may proactively cancel.

- Guidance for 2026 was strong adjusted for historical conservatism – Medpace’s historical guidance has been extremely conservative, almost to a fault. From 2019-2025, Medpace beat its initial EPS guide every year with a median beat of 17% vs the midpoint. For 2026, Medpace guided to a midpoint of ~$17, which suggests “actual” EPS could be expected to come in around ~$20.

- Clinicaltrials.gov has government data on clinical trial starts and cancellations, and you can sort by pharma sponsor. I’ve pulled this data with help from Claude and stripped out the top 20 pharma sponsors to isolate the part of the market that is more relevant for Medpace. While this data is imperfect, it does line up with (a) 2025 actuals – we see an elevated cancellation rate in the Q1 ’25 and Q4 ’25 data and more normal rates for Q2 and Q3, and (b) management’s optimism about 2026 – cancellation rate has been low and new activity robust so far in 2026, with the caveat that the data is very lumpy so March could turn out very different than the below extrapolation of the first 11 days of data.

- We think Medpace has a 5-year compounding algorithm of 15%+ revenue growth (HSD% to LDD% growth in small to mid sized biopharma CRO spend and some market share gains) + moderate margin expansion + capital allocation (buybacks) = 20%+ EPS growth. It’s possible AI begins to have an impact on the clinical trial process and Medpace’s financials over the next five years, in which case we’d expect somewhat lower revenue growth but likely more margin expansion, as lower value parts of the trial are automated by AI and areas where Medpace can flex its therapeutic / regulatory expertise become a higher % of the mix of revenue.

- Home Depot Relative Valuation

- Walmart Relative Valuation

- CVS Relative Valuation

- Goldman Sachs Relative Valuation

- Morgan Stanley Relative Valuation

- Caterpillar Relative Valuation

- Deere Relative Valuation

- Hilton Relative Valuation

- Yum Brands Relative Valuation

- Fedex Relative Valuation

Risks

- Funding environment – biopharma is a cyclical end market highly dependent on the funding environment. Medpace did a good job continuing to grow in 2024-2025 against this backdrop, but Medpace’s growth in any given year will be highly impacted by the cycle.

- Key man risk in August Troendle, who is 69. His level of involvement in the day-to-day decisions of the company (e.g., the daily 10 AM meeting to go over RFP prospects) is unusual for a CEO/founder at this point in the business’ lifecycle. While there are no signs August is going to retire in the near term, at some point this could become a risk / the market could start to question succession planning.

- It’s also worth noting that while we see August as a meaningful positive for Medpace in most ways (his history of disciplined growth + capital allocation is very strong), we have some concerns. August’s personal affairs are intertwined with Medpace – he owns much of the real estate for the company’s HQ, for example, and financed its construction. He is highly aligned with shareholders with the bulk of his net worth in his ~20% Medpace stake, but this kind of business dealing is a yellow flag.

- AI is going to change the CRO industry. Our best guess based on extensive digging into the topic is that the core value-add of Medpace will be largely unimpacted, especially relative to the FSP model of the large CROs that work with large biopharma. We’ve spent time reviewing historical Medpace case studies, and while these are of course marketing documents showing Medpace in its best light, we found it helpful to read through all of the difficulties and logistical complexity that Medpace faces when setting up and executing a trial, especially for rarer indications. However, any shift from the status quo creates risk of disruption, and it is very difficult to say at this stage what the full income statement impact will be on Medpace if AI is leveraged extensively throughout the clinical trial process.

- Two other notes on AI

- Small to mid sized biopharma has been a higher growth part of the industry & the source of major innovation, with large pharma often acquiring biopharma companies with promising INDs. It’s plausible that AI could shift this dynamic, especially if data that may be more accessible to large pharma customers is a barrier to entry, although we could see arguments in both directions.

- One of the large public CROs, IQVIA, has a data business that could give it an advantage in the market if it turns out to be valuable in a world where AI-aided drug discovery becomes a major chunk of the pipeline. It’s plausible IQVIA could use its data business to try to penetrate more of the biopharma market, targeting companies earlier in the process (during drug discovery)